How to choose your accounting firm in UAE: Tax, Audit and Bookkeeping services in Dubai

Not every accounting and bookkeeping firm is licensed to conduct a vast array of tasks.…

The UAE, with its vibrant business landscape, has implemented a new corporate tax regime effective 1 June 2023 under the Federal decree law no. 47. In order to create a fair and seamless transition, the Ministry of Finance and Federal Tax Authority (FTA) have devised a more nuanced federal corporate tax regime, including specialized incentives based on tax profiles.

UAE corporate tax rates applies a tiered rate structure based on threshold and tax brackets of the resident taxable person and non resident juridical persons. Here’s an overview of rates for UAE:

| Type of Company | Tax Brackets | Notes |

|---|---|---|

| Taxable persons | 0% on Taxable income up to AED 375,000 9% on Taxable Income exceeding AED 375,000 | The rates are applied after taxable income is calculated and any exception or reliefs are considered. |

| Qualifying Free Zone Persons (QFZP) | 0% tax rate on qualifying income – Transactions with other Free Zone entities (subject to exclusions) – Income from Qualifying Activities – Qualifying Intellectual Property – Other income within de minimis limits 9% tax rate on non qualifying income including: – Income from Domestic or Foreign Permanent Establishments – Certain real estate income – Non-qualifying IP income | Free Zone entities must meet ongoing conditions to qualify for their Qualified Free Zone Persons status, which means: 1. Business should be registered and operating in a UAE Free Zone 2. Adequate economic substance within the Free ZoneIncome must fall within qualifying categories 3. Non qualifying revenue has to stay below de minimis limits 4. Transfer pricing regulations and documentation apply 5. Audited financial statements are required 5. Required to file returns even on 0% taxable income Losing QFZP status has multi-year consequences (current year where status is lost + following 4 years — total of 5 years.) |

| Corporate Tax Groups | A tax group is taxed exactly like a normal taxable person: – 0% on the first AED 375,000 of group taxable income – 9% on the remaining taxable income | Two or more UAE-resident companies to be treated as a single taxable person for corporate tax purposes, subject to approval by the Federal Tax Authority (FTA). 1. One parent company + one or more controlled UAE subsidiaries wherein parent must hold > 95% (share capital, voting rights, profits/net assets) 2. Tax group files one return via parent 3. Files one consolidated corporate tax return via parent company, who acts as the representative member 4. All members are jointly and severally liable for tax obligations |

Under UAE corporate tax law, a free zone company is treated as QFZP if they fulfill certain conditions, and earns not more than a certain amount of non qualifying revenue.

The de minimis rule sets the threshold wherein Free Zone businesses can retain their QFZP status as long as the non qualifying income does not exceed the lower of AED 5 million or 5% of total revenue, ensuring that all other conditions and requirements are intact.

Once they exceed the tolerated amount, the company will lose their current status within this tax period AND cannot apply for the 0% QFZP regime from the beginning of the relevant tax period and for the subsequent 4 taxation periods, even if income becomes fully “qualifying” again.

| Examples | Revenue Threshold | QFZP Status |

|---|---|---|

| Small Company | Total revenue: AED 2,000,000 – 5% of revenue: AED 100,000 – AED 5,000,000 cap: irrelevant (higher) De minimis threshold = AED 100,000 | If non qualifying revenue is: AED 80,000 → ✔️ QFZP status retained, considering other requirements are fulfilled AED 120,000 → ✖️ QFZP status lost |

| Larger Company | Total revenue: AED 200,000,000 – 5% of revenue: AED 10,000,000 – AED 5,000,000 cap applies (lower) De minimis threshold = AED 5,000,000 | If non qualifying revenue is: AED 4,900,000 → ✔️ QFZP status retained, considering other requirements are fulfilled AED 5,100,000 → ✖️ QFZP status lost |

To further explain this, let’s break it down into two parts: what constitutes exempt income and exempt persons within the UAE CT regime?

| Key Points under UAE Tax Laws | Exempt Income | Exempt Persons under CT LAW |

|---|---|---|

| What is exempted? | 1. Employment income (salary and wages) 2. Personal investment income not connected to a business 3. Capital gains and losses from the sale, transfer or disposal from a participating interest 4. Dividends received from a foreign juridical person are exempt only if the Participation Exemption conditions are met, including: — Minimum ownership (≥5%) or acquisition cost ≥ AED 4 million — Minimum holding period (12 months, or intent to hold) — Subject-to-tax test (foreign tax ≥9% or deemed satisfied) Other specific examples: 1. Qualifying dividends from qualifying shareholdings; capital gains from selling qualifying shares 2. Foreign permanent establishment (PE) income (i.e. foreign taxes paid abroad and PE exemptions) 3. Qualifying intra-group transactions and reorganizations (i.e. asset transfers, internal restructurings) 4. Certain refunds, recoveries and windfalls (i.e. insurance recoveries, refunds or reimbursements, court awards to compensate for losses) | 1. Persons or businesses specifically exempt under the law (e.g. certain government entities) 2. Public benefit entities Specifically: 1. Wholly-owned or controlled UAE subsidiaries of government controlled entities are usually considered as exempt persons unless they conduct commercial activities. 2. Certain extractive businesses (e.g., natural resource extraction) and qualifying public benefit entities can get exemptions if conditions are met. Particularly, businesses engaged in the extraction of natural resources are exempt from CT as these businesses will remain subject to the current Emirate level corporate taxation. 3. Other activities like pension funds, social security funds, and qualifying investment funds may be exempt based on regulatory conditions. |

| How do you treat this in practice? | Income is excluded, but the person is still considered under the corporate tax system | The person is not considered as a taxable person. Meaning, they are outside of scope within corporate tax regime, so they have no taxable income calculation at all. |

Corporate tax is calculated based on Taxable income earned within the tax period. Taxable income generally starts from business profits as shown in their financials. UAE businesses generally follow International Financial Reporting Standards (IFRS) as the accepted accounting framework and follow these global tax standards for preparing financial statements.

Accounting profit is the net profit shown in a company’s financial statements, calculated under IFRS accounting standards, and is the starting point for determining taxable income. With a few tax adjustments, their net profit is then recalculated to arrive at taxable income.

To simplify the manual process for “UAE’s corporate tax calculator”, you can think of taxable income as the amount of what you earned that the government considers taxable. From there, the amount you need to actually pay becomes your tax liability.

You can have taxable income and still end up with very little to none owed liabilities to the government. This happens as the final amount of corporate tax payable once:

It might also help to familiarize yourself with other terms you’ll encounter when fulfilling your tax obligations:

| Terminology | Definition | Where it applies in corporate tax calculation |

|---|---|---|

| Taxable Persons | An individual or entity required to comply with UAE Corporate Tax regime because they carry on a business and related activities | Primarily their business income fuel the CT regime and UAE economy as a result |

| Direct Tax Levied | Direct tax levied refers to a tax that is charged directly on income or profits of a person or business. It is not embedded in prices or passed along invisibly through sales or pricing. | Corporate tax is considered an example of direct taxation on businesses. |

| Withholding tax | A structure where tax is deducted at source and paid to the tax authority on behalf of the taxpayer. | N/A – withholding tax affects cash flow and credits. Depending on the situation, this tax may reduce the cash you receive; be claimed as foreign tax credit, or ignored entirely. |

| Tax Loss Relief | Tax loss relief allows a business that makes a loss in one tax period to use that loss to reduce taxable profits in future periods | This reduces future corporate tax payables by offsetting the loss against future taxable income. In any given future tax period (including 2026), a business can use carried-forward losses to reduce up to 75% of that year’s taxable income before tax. The remainder of taxable income is taxed normally. Example 2026 Taxable profit: AED 100,000 Loss from prior years: AED 200,000 Maximum offset: 75% of AED 100,000 = AED 75,000 Taxable income after relief: AED 25,000 (now subject to CT) |

| Tax Period | The financial year for which corporate tax is calculated and reported | Make sure you are computing and filing for the correct period to avoid penalties |

| Related Party Transactions | Transactions between connected persons or entities that require special pricing and documentation rules | These rules ensure that taxable income reflects market-based profits, not profits shifted artificially between related entities. In practice, they can increase or decrease taxable income through tax adjustments. |

| Transfer Pricing Documentation | These are rules and documents governing how prices are set between related parties to ensure transactions reflect market value | Transfer pricing documentation: – Justifies how prices were set – Supports that transactions are arm’s length – Protects your tax computation from being challenged If documentation supports arm’s length pricing, then your tax computation stands as filed. If documentation is missing or weak, the Federal Tax Authority may recharacterize transactions, adjust income or expenses, and increase taxable income. |

| Arm’s Length Principle | The requirement that related party transactions must be priced as if between independent parties | This applies not just to large companies, but also to: 1. Founders paying themselves 2. Shared services across entities 3. IP licensing between related companies Size is not an exemption for this principle. |

Here’s the step by step guide for corporate tax calculation under UAE CT Law:

NOTE:

For deductible costs, here’s a simple test you can use to ask to determine whether the expense qualifies. You can ask the following questions:

If the answer is yes to all three, it is generally deductible.

To ensure your books are clear and up to date, it is best practice to also calculate your profit after taxes.

In the event that you record a loss in your filed returns, you can claim it by adding in the Corporate Tax return itself.

To claim tax loss relief in 2026 and beyond, the following conditions must be met:

In order to claim it, you must:

Here is a summary of the calculation formula that applies to majority of companies under the standard tax regime, including tax calculator examples and some specific conditions that add a complexity layer into how a taxable person’s accounting income is calculated.

The formula follows all taxable persons, including freelancers, free zone entities, and entities earning worldwide income (i.e. all income a person or business earns anywhere globally, and not just within UAE).

| Type of Example | Description of Context | Computation | Note |

|---|---|---|---|

| Freelancer monetizing multiple income streams Important note: if you’re a natural person with turnover ≤ AED 1 million, CT does not apply at all. A natural person may also elect a Small Business Relief if turnover/revenue ≤ AED 3 million, subject to conditions (check our guide here). | Sample income streams: ✔️ Monthly client retainer for A, B, and C: AED 920,000 ✖️ Salary income of AED 15,000 ✖️ Income on dividends and savings: AED 30,000 ✔️ One-off strategy project: AED 90,000 ✔️ Paid online workshop (self created): AED 80,000 ✔️ Speaking honorarium related to business opportunity: AED 30,000 TOTAL BUSINESS INCOME: AED 1,120,000 Expenses Deductible expenses (marketing, subscriptions, co-working): AED 140,000 Nondeductible expenses: AED 40,000 total Personal phone partly claimed: AED 15,000 Personal travel: AED 25,000 | Total Business Income: AED 1,120,000 Step 1: Accounting profit (Income – Expenses) AED 1,120,000 − AED 140,000 − AED 40,000 = AED 940,000 Step 2: To get taxable income: Add back nondeductible expenses: AED 940,000 + AED 40,000 Taxable income = AED 980,000 Step 3: Tax liability 0% on first AED 375,000 → AED 0 9% on remaining AED 605,000 → AED 54,450✅ Corporate tax liability: AED 54,450 | In this example, we show that: 1. Accounting profit is not necessarily equal to taxable income 2. Salary and Personal income is not included in corporate tax calculation 3. Small nondeductible expenses can significantly change the payable 4. The threshold of AED 375,000 softens the impact for smaller enterprises, but does not remove filing |

| UAE Mainland Startup (LLC)B2B SaaS productFirst full year of operationsUses accrual accountingNot in a Free Zone, no special exemptions | Revenue Annual recurring revenue (subscriptions) including global client subscribers: AED 1,200,000 Expenses (total: AED 850,000) – Salaries and founder compensation: AED 450,000 – Cloud hosting and software tools: AED 120,000 – Marketing and sales: AED 180,000 – Office, utilities, admin: AED 70,000 – Nondeductible items (e.g. penalties, personal expenses booked): AED 30,000 | Step 1: To get the accounting profit Accounting profit: AED 1,200,000 − AED 850,000 = AED 350,000 This is the profit shown in the financial statements. Step 2: Taxable income Add back nondeductible expenses: AED 350,000 + AED 30,000 Taxable income: AED 380,000 Step 3: Apply corporate tax rates 0% on first AED 375,000 → AED 0 9% on remaining AED 5,000 → AED 450 ✔️ Final corporate tax liability AED 450 | This example shows clearly that: !. A startup can generate over AED 1 million in revenue and still pay very little corporate tax if margins are thin. 2. You can use Small Business Relief given this falls below <AED 3 million revenue. Be mindful however that this is not beneficial to do if you have losses as they will not be recoverable. 3. Even when tax payable is minimal, the startup must: -> Be registered for Corporate Tax -> File a Corporate Tax return on time |

| Qualifying Free Zone Company with mixed revenue | – Qualifying Income taxed at 0% – Other income (not qualifying) taxed at 9% – De minimis test is revenue-based: lower of 5% of total revenue or AED 5,000,000 -Assume QFZP conditions are met (substance, audited FS, TP, etc.) | Revenue inputs (used for de minimis test only): -> Qualifying revenue = AED 6,000,000 -> Non-qualifying revenue = AED 200,000 -> Total revenue = AED 6,200,000 De minimis threshold = lower of (5% × 6,200,000 = AED 310,000) or AED 5,000,000 → AED 310,000 ✅ Since AED 200,000 ≤ AED 310,000 => de minimis not breached. Tax computation: Step 1: Start from Accounting Profit Step 2: Apply CT adjustments to get to Taxable Income. Step 3: Allocate taxable income between Qualifying Income (0% tax) and other income that is not Qualifying Income (9%) Note: allocation is based on tagging income streams (not proportional allocation by revenue unless it reflects the actual nature/source) Step 4. Calculate corporate tax payable (Qualifying taxable income × 0%) + (Non-qualifying taxable income × 9%) | In this example, we show that the tax rates apply only after taxable income is calculated. Revenue alone is never taxed. |

When calculating under UAE corporate tax, businesses must adjust their profit before tax to reflect what is allowed or disallowed under tax law. These tax adjustments ensure that corporate tax is applied to the correct figure rather than what appears in the financial statements.

Key adjustment areas include:

Accurate classification of expenses for all business partners is essential to avoid overstating or understating taxable income, which can lead to errors in filing and potential penalties.

For QFZP status, a simple rule of thumb is:

NOTE:

Small Business Relief (where applicable)

Eligible small businesses (with revenue ≤ AED 3 million) may elect for Small Business Relief, which can reduce taxable income to zero (i.e. no taxable income) for the relevant tax period. However, this relief does not remove the requirement to register for Corporate Tax or file a return.

Small Business Relief under the UAE Corporate Tax Law is only available for tax periods starting on or after 1 June 2023 and ending on or before 31 December 2026.

Some businesses use corporate tax calculators as a references, but our main advice with our clients is that calculating corporate tax must always align with financial statements and filing requirements.

We understand that for non tax professionals, calculating corporate tax can be overwhelming and tax in the UAE requires focus and expertise. It helps to prepare ahead of time by using the standard accounting systems, keeping clean records of internal working papers, and treating this as a continuous cycle fixed by adding correct tags early on.

skrooge.ai can help you with expert tools that allows you to tap into qualified tax advisors that gives professional advice on corporate tax purposes. We provide services with transparent fees.

Your СT filing on autopilot, at no extra cost, with 100% of transactions/documents checked:

To learn more about our services specific to corporate tax, visit our website. You can also check your pricing based on monthly transactions.

Questions? Contact us any time.

This article provides general information on UAE Corporate Tax and does not constitute tax advice under applicable laws. Corporate Tax treatment may vary depending on individual circumstances. Readers should seek professional advice before making any decisions.

Under the Federal Decree Law No. 47, businesses are subject to UAE corporate tax regime effective 1st of June, 2023. To administer and track this transition, Ministry of Finance and the Federal Tax Authority (FTA) have devised a fair structure for businesses operating in the UAE.

In the corporate tax law, different types of entities are subjected to different tax brackets and incentives, depending largely on whether their income is exceeding AED 375,000 or under the conditions of the Qualified Free Zone entities.

For taxable persons, the corporate tax rate is at:

0% rate on taxable profits up to AED 375,000

9% rate on taxable profits above AED 375,000

For Qualifying Free Zone Persons:

0% on qualifying income and 9% on non-qualifying income

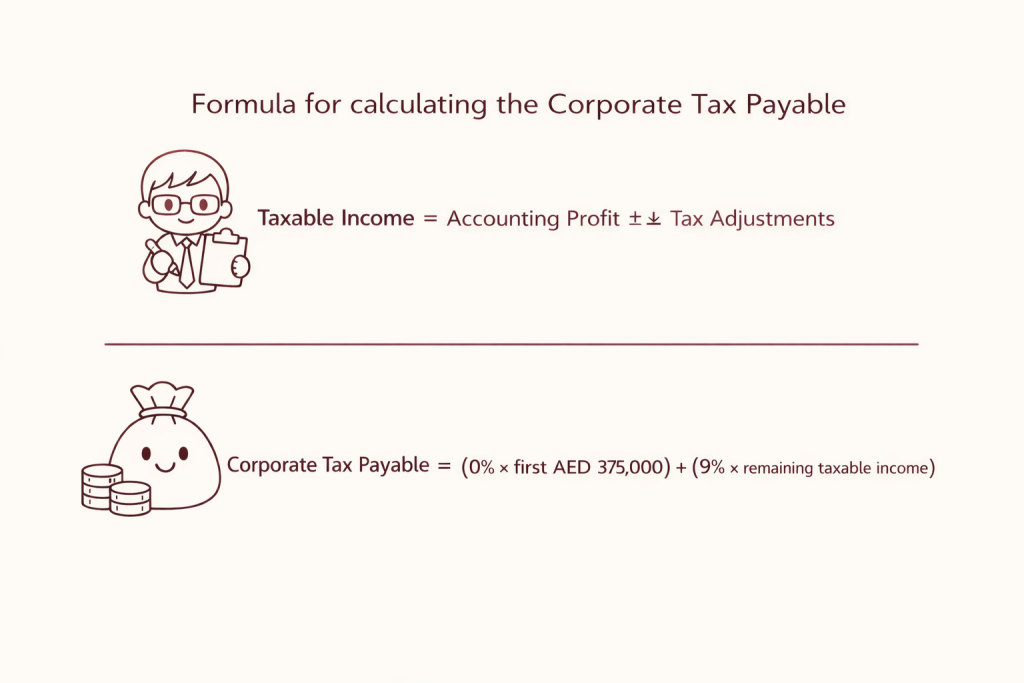

To simplify corporate tax calculation, you can use the following formula to arrive at the corporate tax payable:

1. Determine the profit indicated in your financial statements for the specific financial year (i.e. Business Income – Total Expenses)

2. Taxable Income = (Business Income – Total Expenses) + Nondeductible expenses ± Tax Adjustments

3. Business profits tax (CT) Payable = (0% x first AED 375,000) + (9% x income exceeding AED 375,000)

-> Taxable persons with income exceeding AED 375,000: subject to 9% tax

-> Taxable persons with income less than AED 375,000: subject to 0% tax bracket

This typically includes business costs that are incurred wholly and exclusively for the purpose of generating income under their commercial activities.

Allowable deductions include:

✔️ Employee salaries, wages, bonuses, benefits, mandatory employment charges and training costs related to business operations

✔️ Office and running costs including rent, service charges, utilities, office supplies, coworking space fees

✔️ Professional and outsourced services – accounting, audit and bookkeeping fees, legal and compliance costs, consultancy and advisory fees, and IT support and managed services

✔️ Sales, marketing, operations, IT and finance related expenses

✔️ Depreciation and amortization of business assets

Expenses that are only partially deductible – these must be apportioned between business and personal use:

✔️ Mobile phone and internet used for both work and personal matters

✔️ Vehicle expenses used for both business and private travel

✔️ Home office costs (where applicable)

Only the business portion is deductible.

You start by accessing the company’s financial statements for the relevant tax period, then you apply the formula to arrive at your tax liability.

To arrive at the tax payable in the current financial year, use the following rule of thumb in your tax calculator:

1. Add back nondeductible expenses – expenses that reduce company profit but are inadmissible from tax

2. Adjust for partially deductible costs

3. Remove other exempt and excluded income (for example, dividends)

4. Cap interest expenses on shareholder loans and other financing costs by adding back the disallowed portion of the expenses

5. Account for depreciation, related party pricing adjustments and other carried-forward losses from prior years.

Corporate tax in the UAE has exemptions on income. Similarly, certain persons or businesses are exempt under the law (e.g. certain government entities or public benefit companies).

Specifically:

1. Wholly-owned or subsidiaries of government controlled entities are usually considered as exempt persons unless they conduct commercial activities.

2. Certain extractive businesses (e.g., natural resource extraction) and qualifying public benefit companies can get exemptions if conditions are met. Particularly, businesses engaged in the extraction of natural resources are exempt from CT as these businesses will remain subject to the current Emirate level corporate taxation.

3. Other activities like pension funds, social security funds, and qualifying investment funds may be exempt based on regulatory conditions.

A Free Zone Person may qualify as a Qualifying Free Zone Person (QFZP) only if it meets the conditions set out under the UAE Corporate Tax rules (and does not elect to be taxed under the standard Corporate Tax regime).

Under QFZP, free zone registered companies can claim 0% taxes on qualifying revenue and 9% on non qualifying revenue. To determine qualifying vs non qualifying, the nature of the revenue must satisfy the requirements, regardless of company structure.

To stay compliant, you must be able to trace income by showing:

✔️ who the customer is

✔️ where they are established

✔️ whether they classify as free zone, mainland or foreign entities

UAE Corporate Tax returns and any payments must be made within 9 months after the end of the tax period, regardless of profitability. Late filing or payment can result in administrative penalties, even if no tax is ultimately due.

It is administered under the EmaraTax portal, an official platform managed by the Federal Tax Authority.

Thank you!

We've received your request and will get back to you shortly.

Loading...